Why everyone is saying no to the Big 12's capital infusion deal on the table

(Before we get into this, can we give a shoutout to the evolution of the AI Slop Machine? Look at that feature image generated by ChatGPT's new image module. This isn't a sponsored shoutout, but boy it could be. Hit us up, Sam.)

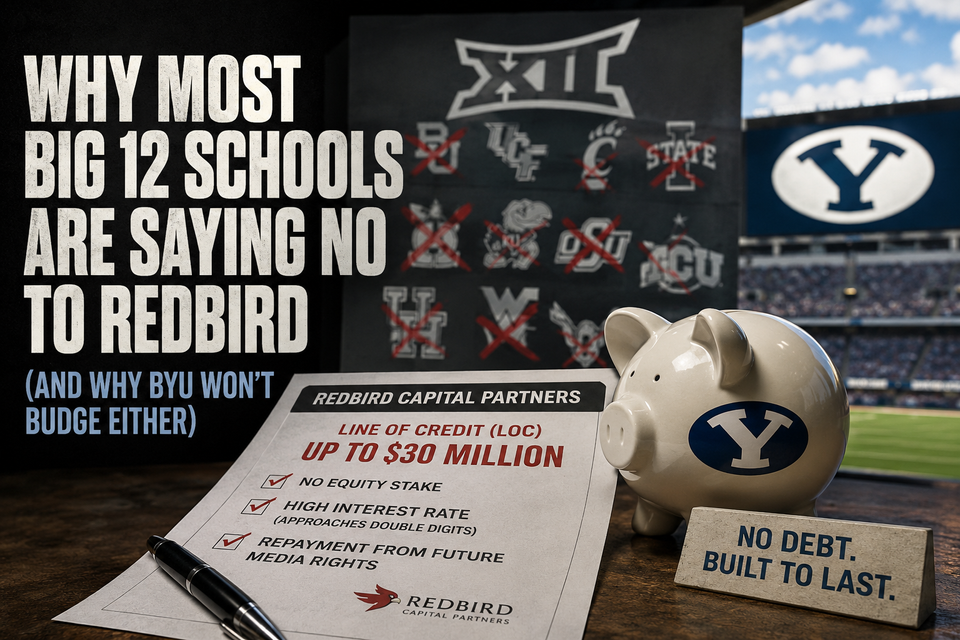

About two weeks ago, the Big 12 Conference announced a private capital deal with RedBird Capital Partners. The deal provides the Big 12 Conference with a $12.5 million capital infusion to help generate additional commercial revenue. The deal also allows each member school to have access to a line of credit (LOC) up to $30 million for each university. In a time where money is tight, NIL is looming, and every college athletic program in the country is looking for any money they can find, this deal seems like a little bit of relief for Big 12 schools.

And two weeks later, nobody is biting on the deal. In fact, the majority of Big 12 schools have publicly declined any LOC from RedBird. Utah, Kansas, and Arizona State are the only three schools who have not stated what they intend to do.

Why aren’t schools taking the money? Times are tough, the Big Ten and SEC continue to make more and more money, and 13/16 Big 12 programs have already rebuffed the idea of $30 million from an external party. Why?

Some particulars of the deal:

This is not a typical private equity deal where schools are selling away aspects of their athletic program in exchange for cash. This is truly a LOC that approaches a double-digit interest rate on all funds that are borrowed. There have not been any public reports that the terms of the deal show any way that RedBird can gain any equity stake in any University athletic program. This is important. Big 12 schools would not be selling themselves or adding seats to their Board of Regents if they accepted money from RedBird.

If a school does opt into the deal, they are effectively mortgaging away future media rights. They get access to the RedBird LOC, and any repayment + interest would be distributed when the school receives their media rights payout from the Big 12 Conference. The flow of funds would look something like this: TV Network > Big 12 > RedBird LOC Payment > University. There aren’t monthly payments like your consumer credit card. The payments come via the conference in the name of the university when disbursements are being made. So, the likelihood of default is exceedingly low, but not zero.

The deal seems reasonable enough, right? Keep all of my equity and get an advance of my future earnings to help stay afloat during uncertain times.

So, why are so many saying no?

Let’s be clear about one thing: Schools are not saying no because they suddenly found a moral compass against private equity entering college sports. If you run across any fans on social media making that claim, you can kindly scroll on because it’s simply not true. And yes, my fellow Cougar fans, I know what you’re about to say, but bear with me for a few more paragraphs before you say it.

Let’s bring this whole scenario a little closer to home with a real-world example of the decision these schools are making right now. I’ll use my own life as an example.

In 2016, I bought my first house. It felt like housing was expensive at the time, but five years later, I sold my house for nearly double what I had paid for it in 2016. What’s more, when I rolled that equity into the purchase of a new home, I got an even better interest rate on the new mortgage in 2021. My monthly mortgage payment stayed roughly the same and I got a brand new house with more rooms and more space for my growing family.

But now it’s 2026. I’m still in the same house, and I probably will be for a long time. Interest rates have tripled since I moved into my house, and property values continue to climb and climb. Even though I’m five years further into my career, the economics of moving into a nicer home simply do not make sense.

And this brings us back to the RedBird deal. Schools aren’t afraid of private equity (at least not afraid enough to say no to money), but rather, they are looking at the terms of the deal and deciding they can do better elsewhere. “Better” might not happen today or tomorrow, but the economics don’t make sense today, so they are waiting for a time when they do.

Unless a school NEEDS the money right now, they can afford to wait. The RedBird deal will still be available to them down the road, if not from RedBird then from someone else willing to match similar terms.

This makes Utah’s situation especially interesting.

Utah has yet to publicly reject the deal, while exploring a separate capital deal from Otro Capital. That does not automatically mean that Utah is desperate for cash and bleeding, but it does suggest a level of financial urgency that others in the conference might not currently feel.

Okay, so BYU is saying no because they don’t see the financial urgency then?

BYU’s financial situation certainly makes saying no to this LOC easier, but there are a lot of things pointing to BYU making the same decision regardless of present circumstance.

Last month, BYU athletics director Brian Santiago was on The Divot Podcast talking about BYU and Private Equity. He didn’t mince even a syllable when he said, “I think we can reasonably say private equity will never be a part of the sports program at BYU. That’s something that everybody knows [that we will not participate in private equity]. And, when it comes up in the room, even in the Big 12 room as they have looked at a lot of different things, it’s pretty clear, and I just remind everybody that BYU will not be participating.”

Every BYU fan knows that, but it’s worth digging into a little bit more. The firm stance, especially in relation to the RedBird deal on the table right now, is consistent with the broader philosophy The Church of Jesus Christ of Latter-day Saints teaches about debt: Don’t get in it.

BYU (the University, the AD, the anything) does not borrow money.

“That’s a strength for us. Our governing board is for us, very, very important, and we’re going to live within the principles that we’ve been taught, and we’re having great success doing it that way,” Santiago said.

So, yeah… that seems pretty clear.

It will be fascinating to follow what happens from here. If none of the Big 12’s 16 schools opt into this deal, it will be another failed endeavor for innovation from Brett Yormark. The Big 12 Commissioner is constantly trying to push the needle and find ways to generate more revenue. Whether it’s games overseas or glass floors with more ad space, Yormark wants to push the needle and is not afraid of being a pioneer. But so far, his member schools seem to be saying they’d prefer a little less pioneering and a little more certainty before jumping in.

That makes sense to me and my house.